INDIA: SNAPSHOT

MoreFDI In India

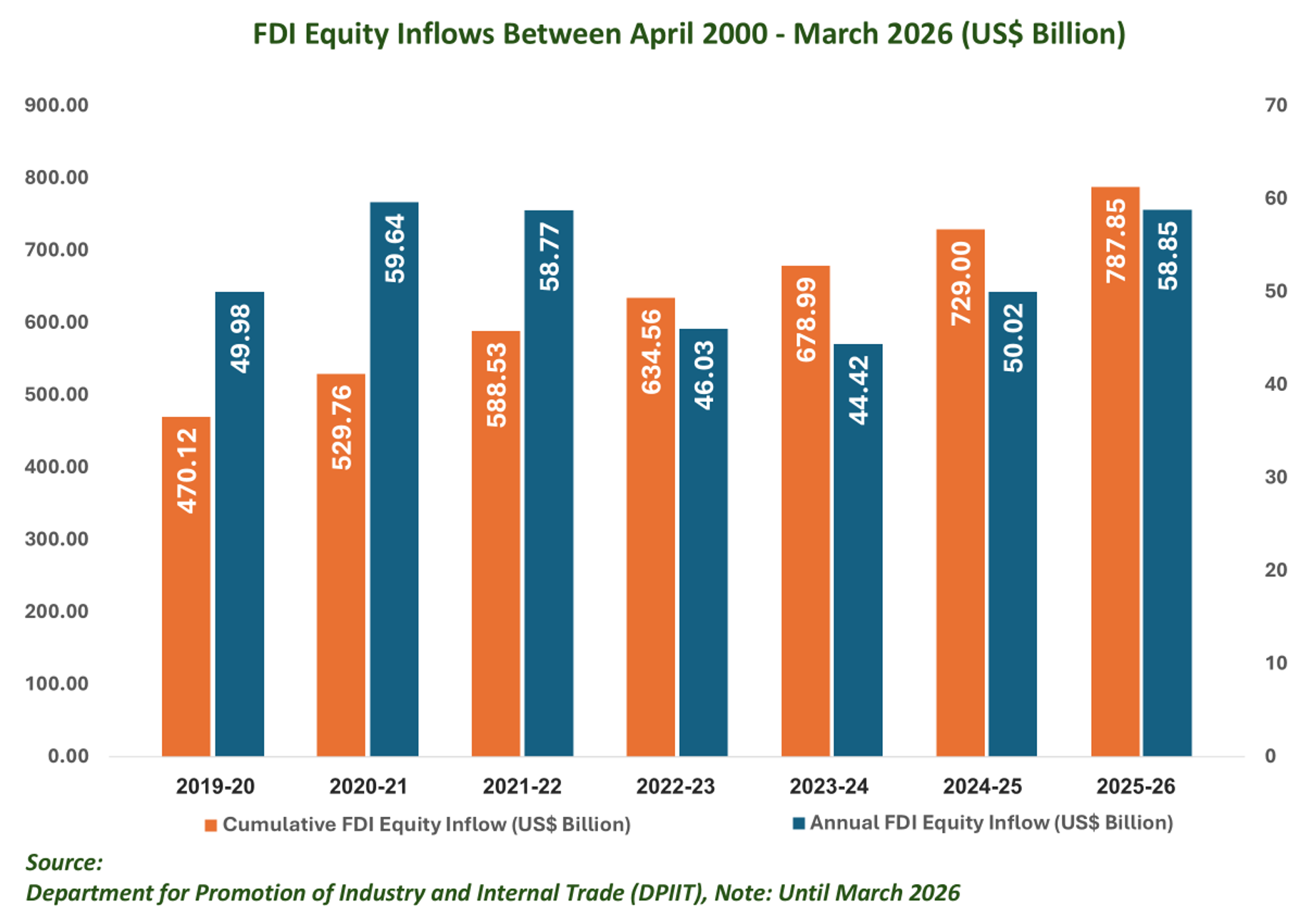

According to the Department for Promotion of Industry and Internal Trade (DPIIT), India's cumulative FDI inflow stood at US$ 1.16 trillion between April 2000-March 2026, mainly due to the government's efforts to improve the ease of doing business and easing of FDI norms. The total FDI inflow into India in FY26 stood at Rs. 8,25,485 crore (US$ 94.52 billion) and FDI equity inflow for the same period stood at Rs. 5,16,936 crore (US$ 58.85 billion).

NEWS

07

August

2026

April–July 2026: India’s Steel Sector Exhibits Growth Trend...

Read More

07

August

2026

India and South Africa expand cooperation in critical minerals, pharmaceuti...

Read More

07

August

2026

Auto sales hit record 2.59 million units in July, rise 26% year-on-year...

Read More

FII (Foreign Institutional Investors)

Partners